Semiconductor Equipment Supply Resilience in MENA.

Industrial trendsMENAequipmentresiliencesemiconductor supply

This report explores the resilience of the semiconductor equipment supply chain in the MENA region amidst global challenges and opportunities. It highlights the strategic role of MENA in the global semiconductor supply chain, focusing on regional growth prospects and infrastructure developments. The report provides an in-depth analysis of market trends, government initiatives, and regional disruptions affecting the semiconductor equipment sector. It recommends strategies for enhancing resilience and competitiveness through investment, policy frameworks, and technological advancements.

Vivek Goswami, Ghost Research

October 2025

Perspective.

PurposeTo assess the resilience and growth potential of the semiconductor equipment supply chain in the MENA region.

AudienceIndustry stakeholders, policymakers, investors, and researchers interested in the semiconductor and technology sectors.

Special EmphasisTechnology adoption, government initiatives, and supply chain resilience.

49Pages of Deep Analysis

116Curated Credible Sources

1Proprietary AI Visuals

1Data Analysis Tables

$495

Vivek Goswami

11+ Years of Experience

Sectors & Industries

IndustrialsConsumer StaplesEnergy

Functions & Expertise

Market IntelligenceStrategy & GTM

Have questions? Our Research Desk is here to help

Top Insights.

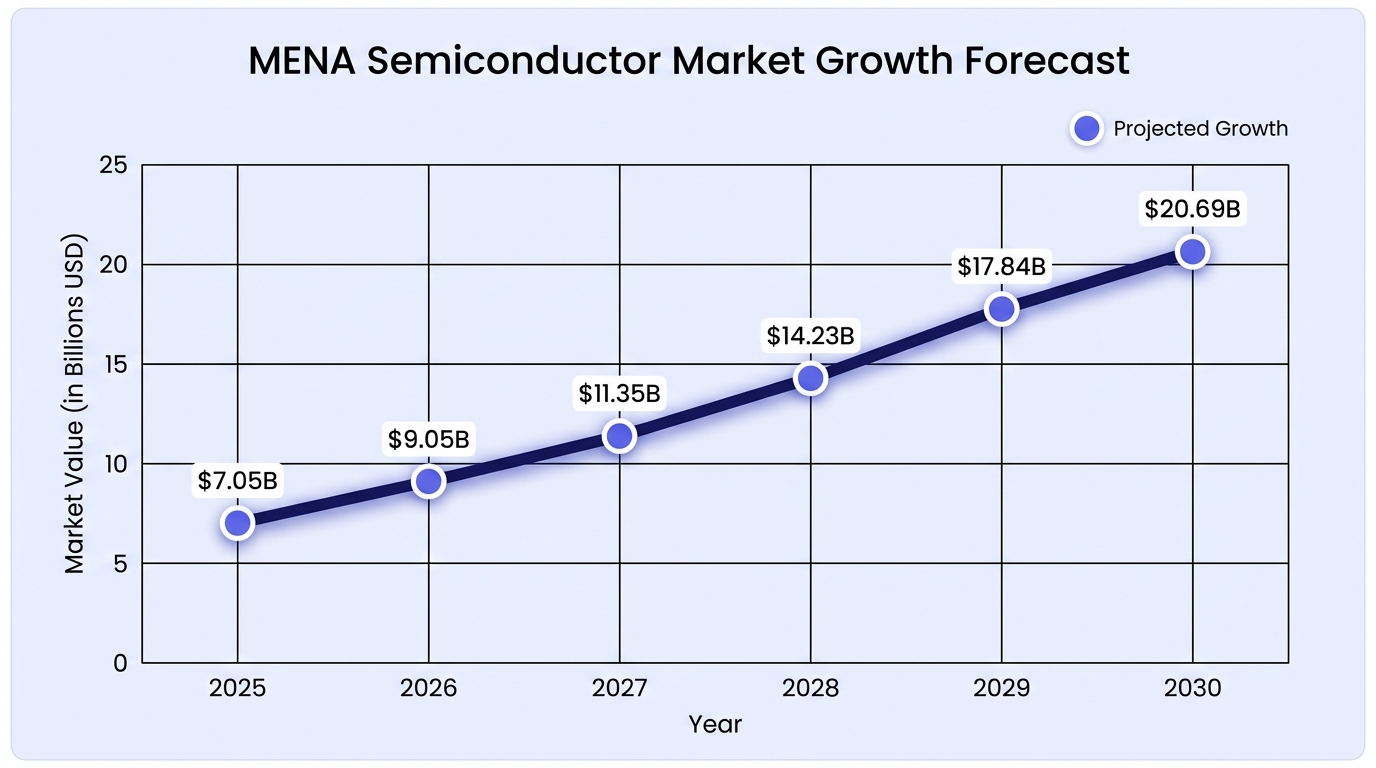

The MENA semiconductor market is projected to rise from $7.05 billion to $20.69 billion by 2030.Geopolitical instability and logistical constraints remain key vulnerabilities for the MENA supply chain.AI chip demand in MENA is expected to grow significantly, reaching $16.85 billion by 2030.There is a notable shortage of skilled semiconductor engineers in MENA, with a gap of 50,000 to 70,000 professionals.MENA relies heavily on imports for semiconductor equipment, with limited local production capacity.Key Questions Answered.

49Pages of Deep Analysis

1Proprietary AI Visuals

116Curated Credible Sources

1Data Analysis Tables

Summary.